MERGERS & ACQUISITION EXIT

Historically, the large majority of technology startup exits have occurred by selling the business to a third party. The investment banking terminology, M&A, for Mergers and Acquisitions, has been universally adopted in the technology world to convey the sale to a corporate buyer. An M&A event can be driven either by an acquirer or by a seller (the startup shareholders). In any case, it is advisable to have a plan in place.

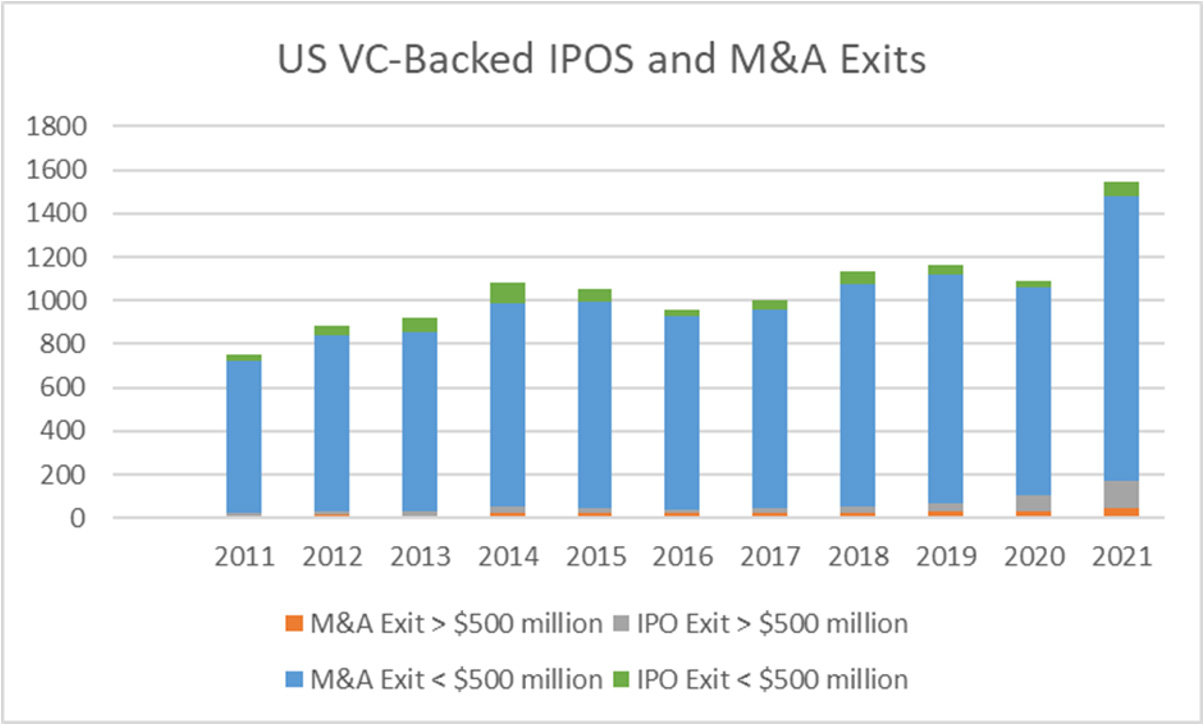

From data provided by PitchBook reproduced in NVCA 2022 Yearbook

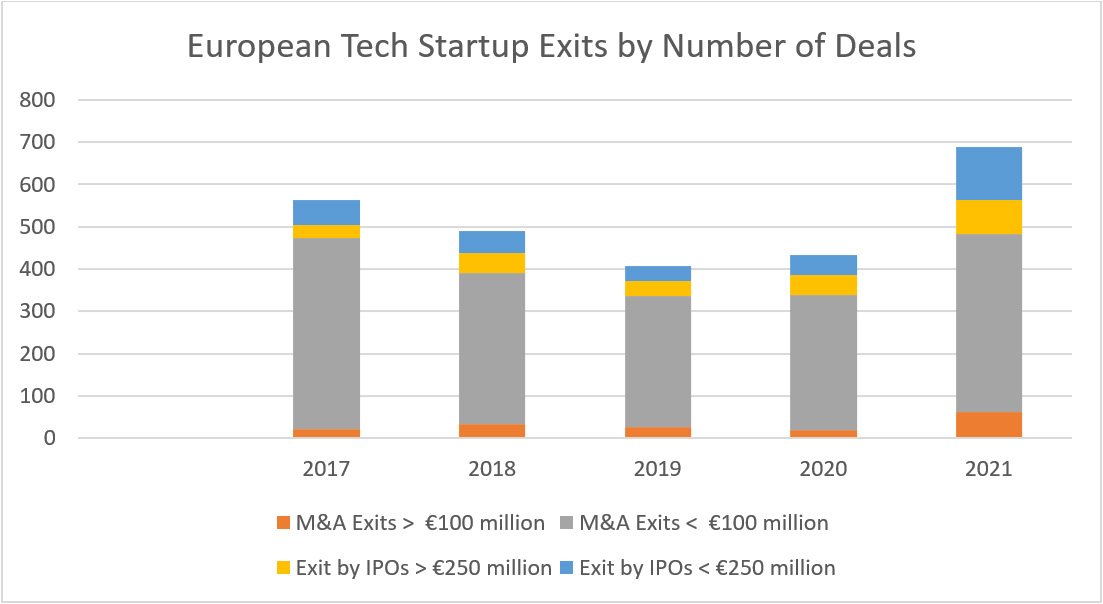

Source: from Atomico data in State of European Tech 2021.

When the doors to IPOs are closing for lack of appetite from investors, as is the case at present, high technology entrepreneurs may turn to finding a buyer for their business, either a corporation that would absorb the company, legally a merger, or a private equity fund that would act as owner/investor with the goal to divest at a profit, referred to as a buy-out transaction.

Buyer’s Unsolicited Interest Versus Seller’s Search for Potential Buyers

Though the result may be the same -the sale of the business-, attracting unsolicited interest from a corporate buyer or an investor may catch you in the dark, completely unprepared, whereas searching for a buyer involves steps you deliberately take after weighing pros and cons of a sale and deciding the timing is now. Because you are most likely surrounded by investors in your firm, the decision to respond to an unsolicited interest does not rest in you but in the board of directors, or the supervisory board. Conflicts often arouse between founders and investors when no exit strategy had been agreed at the time of the investment. Successful businesses have aligned interests between founders and investors as much as possible (see our Blog) and generally together they tend to decline spontaneous offers from third parties as they foresee a higher long-term return by proceeding with the execution of the internal ambitious plan they all signed for. There are some rare exceptions.

Why sell?

- Are you forced to exit by investors? Investors that need an exit, when their fund require a liquidation, are the ones behind the decision to sell one of their portfolio companies.

- Are you burnt out? Is your vision blurred and you have lost the magic to find a brilliant way forward?

- Do you think you deserve to cash in after so many years of hard work, sacrifices, and want to enjoy life as pictured in Conde-Nast magazine?

- Do you suddenly want to undertake a completely different project and build a new business from it?

- Do you think the timing is too good not to put your company for sale, since revenue and profit have skyrocketed, and you sense it is unlikely such a fast growth will continue in further years?

All these are legitimate reasons to envisage a sale of the enterprise.

Why It Is the Second-Best Exit Option for Founders

Entrepreneurs rarely sell their company at a price equal to what an IPO price would provide, when IPOs are possible. Only in cases where two or more potential buyers bid to acquire the business, a price war ensues which may result in a handsome bounty for sellers. It is a second-best option not only for the money returned to entrepreneurs, but also because it brings the end of the dream of accomplishing the entrepreneur’s vision further. Some entrepreneurs would be content to halt their journey in a business if its integration within a larger enterprise with hard-to-find capabilities allows to move the vision beyond its original aspiration.

How To Select the Buyer If You Want Your Dream to Be Pursued?

There is no such thing as a merger of equals. The ideal situation is to be discovered and lured by a potential buyer. In the other way around, the buyer is in a position of strength in the negotiation process. In the latter case, you are seeking to arouse interest by multiple potential acquirers to maintain some competition in the deal. The first circle you must search from is among businesses that complement your enterprise activity, as the purchase would enlarge their offer to the market, and businesses that could use your technology in fields you have not explored. A good understanding of the target buyer’s culture is important, as, by selling the business to them, you entrust the team that helped you reach this significant step to their hands. Buyers are motivated to keep key talent, especially in deeptech, where knowledge of the technology is paramount. A seller would be well advised to scrutinize all past transactions made by potential buyers. Some are known to acquire and kill, to protect their existing, older, technology and eliminate a threatening future competitor. Last, mixing a fast-paced business with an established company is a very hard act. Even a superb planning cannot always yield a success. Entrepreneurs who scoff at it, using the ‘take the money and run’ attitude, do it at their peril. They find out when they try to build a team for their new venture.

The Process

M&A is not a simple process, and it takes a long time to be accomplished successfully. Getting fit and ready for a sale requires some steps to follow diligently.

- Map a broad ecosystem, highlighting many (cash-rich) companies.

- Make your due diligence on at least 15 target buyers: detailed activity, business model, technology, talents, competitors’ strategies.

- Craft a custom-made presentation of your business targeted to each of those companies with a value proposition making a deal appear indispensable, either as an offensive strategy or a defensive one.

- Value-price your company, as you would do for a product. Forget about traditional valuation tools. A corporate buyer does not acquire a company for its flow of discounted cashflow. It buys it because it will help it change scale, dominate a market, annihilate competition, dictate prices or thousands of other reasons that are more relevant to its business than an expected financial performance.

- As a last resort, you can reach out to your competitors. Generally, I refrain from advising it, as competitors will demonstrate interest with the goal to acquire as much data on your business as possible, some of which they could use to correct their own strategy, and ultimately decline an interest as a buyer. Even with a good legal team at your service, it is an uphill battle to keep important commercial and strategic data protected.

- Hire an investment bank that has expertise in your space and does not spend weeks in elaborating gigantic models to articulate a price. Selecting the right investment bank is no picnic. Sometimes an obscure, small investment bank may have among its team an investment banker who is the perfect fit, having developed an inside knowledge of the industry and accumulated an unparalleled rolodex of entrepreneurs and executives. As long as there is no conflict of interest, this is the bank to hire. The investment bank develops the information memorandum on the company, putting its name and reputation behind the quality and veracity of the document. This document is provided to potential buyers that have agreed to sign a non-disclosure agreement (NDA). As for legal documentation necessary to close a transaction, the buyer’s investment bankers will interface with the seller’s bankers. It is advisable to put a cap in time for these exchanges, otherwise you may have no visibility as to the closing while you may be forbidden to entertain concurrent approaches.

- Build the comprehensive due diligence package on the company, following the advice of your legal counsel and investment banker, to be provided to companies that have signed a letter of intent, a non-binding agreement. This step is now done online, through a virtual room, with access codes.

What if it is a Private Equity (P.E.) Buyer?

P.E. are institutional investors with in-house expertise in one or more industries, have access to a vast network of operating talent and generally put their resources to accelerate the creation of value with a full control of funding and use of proceeds. Their goal is to sell within 5 to 7 years, multiplying their price comfortably. They have the same options than entrepreneurs as to their potential exit, an IPO, M&A or a Buy-out. In the last twenty years, the latter case has developed significantly. I know a company that had four successive PE owners and is still thriving with a pivoted strategy.

I would advise that entrepreneurs cut any link with their previous enterprise after the transaction, even as a consultant to the new owner. For the company, for the new owner and for the ex-entrepreneur, a clean slate frees each party of discomfort and emotion.

Timing to Exit

Entrepreneurs need to assess at what stage the value they create is diminishing. This tipping point is the theoretical best timing to sell in terms of financial return. As future growth is a big factor in valuation, there is an optimum when an exit yields the maximum value. To illustrate the point in a gross schematic way, selling a company with $3 million net income and a 40% estimated growth in year 1 followed by a 30% growth in year 2 and 20% in year 3 could fetch approximately $120 million in year 0; if sold at the end of year 1 it could fetch $126 million and $109.2 million at the end of year 2, if we apply a gross multiple equal to the growth rate. There are of course other factors than the growth rate that determine the price.

Terms to Watch For

- Price: sellers seek to obtain the whole amount at the closing, when buyers tend to split the price in a fixed amount paid at the closing and an amount based on future results, the earnout. Though a very successful acquisition can bring a higher value to the seller, it is rightly argued that earnings generated after a take over are totally dependent on the new management and on the level of synergy between the two merged entities. The seller has no longer a say in it.

- Indemnification provision: it is a Pandora’s box. The buyer, despite a high scrutiny of all due diligence documentation, fears a lack of disclosure on aspects that prove to be critical in the health of the acquired business. There is generally a threshold amount of losses, called the basket, before the indemnification by the seller is activated. Such indemnification must be capped, giving the seller an understanding of the maximum incurred financial risk.

- An alternative to the indemnification is a Representations and Warranties Insurance. It eliminates or reduces escrows or contractual indemnities for sellers, replacing them with an insurance policy.

- Incentives to maintain critical employees. Buyers need to avoid the drain of valuable talent, indispensable for the transfer of knowledge and the stability of the firm.

Conclusion

Entrepreneurs must always be prepared to address an M&A event. If recent transactions are setting a trend, technology companies that have hardly completed a Series A financing find themselves courted by big predators, whether traditional businesses or major technology leaders. No outside advisor should advocate for or against such transactions, as each case is unique. When the founder of Snapchat turned down a $3 billion offer from Facebook in 2013, analysts ridiculed his arrogance. Eight years later, Snapchat was valued at $136 billion, more than 40 times Facebook’s offer, while Facebook (Meta) stock price, during the same period, increased by a factor of 9. Even after the fall of NASDAQ in 2022, as of today, the ratio stays in favor of Snapchat (x11 vs. x4.5).

If an entrepreneur is building a long-term business based upon a growing vision, selling is not an option. However, the same entrepreneur must deal with its investors. Even when the public market is reluctant to accept new technology companies, it may be worth to price an IPO at a low multiple. If the execution of its ambitious plan goes well, public investors will take note. The other option is to try to find new investors to buy-out those in need of an exit.

M&As are long and expensive, yet they are a necessary step for most entrepreneurs who have reached a certain status, an achievement that concerns only a happy few among those who start a technology business.