ADAPT OR PERISH

Closing financing rounds have become harder in the last two years. Stars of yesterday that raised huge amounts of cash are now drifting, some are folding, like Convoy, valued at $3.8bn in 2021. The pendulum of the private capital market has moved from an entrepreneur’s market to an investor’s market.

a. Never underestimate the high dependency of startups upon the economic outlook

This is counter intuitive. One would surmise that businesses built with technologies bound to disrupt legacy businesses are shielded from the vagaries of the capital markets. Even investors who are investing their own money are affected by cycles. From private equity investors down to founders seeking pre-seed money, it is a chain reaction born from the public stock market behavior. Public equities and bonds, because of their high liquidity, are held universally.

Venture capital firms, particularly those with non-stellar returns, experience hard times to raise financing for their upcoming funds. First tier VCs who until 2021 were pouring loads of cash on startups are holding their hoard of money close to their chest.

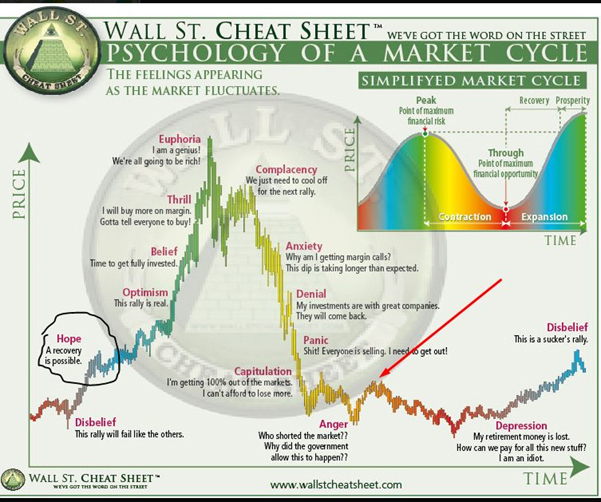

i. Uncertainties trigger a sell-off on the main capital markets, led by NASDAQ.

After 3 years of euphoria when NASDAQ grew at a compound annual growth rate of 32.95% from early 2019 to the end of 2021, investors’ optimism has been replaced by caution. When NASDAQ is going up, private investors in startups enjoy multiple exits for their investments; the floodgates open wide for IPOs. When NASDAQ is going down over a significant period, the floodgates close. Venture capitalists then shift their focus to the best companies in their portfolio, reducing their interest in new investments to almost nothing. Hence entrepreneurs need to appreciate the dynamics of fund raising.

It is impossible to predict whether it is the start of a long cycle or whether there are reasons to believe that the situation will quickly improve. As a reminder, it took seventeen and a half years after the peak of March 2000 for NASDAQ to register a new high.

ii. Entrepreneurs spend more time convincing investors.

It takes much more time for founders and CEOs to raise funds. Criteria to attract investors have changed. Family offices, confident with their long-term view, take a bigger role in some early-stage funding. Startups that have not executed their plan with success are out. In some respect, the survival of the fittest is the rule for both startups and investors. Shouldn’t it be always the case?

iii. Skyrocketing valuations are now vintage curiosities.

Exits for VC-backed companies reached an all-time high in the U,S. in Q3 2021. Concurrently the median valuation for each round also reached all-time highs, after respective compound annual growth rates (cagr) of 16.7% for seed rounds, 27.9% for early stage and 31.8% for late-stage rounds during the period 2019-2021. (Source: PitchBook/NVCA).

iv. The message from investors to their existing portfolio companies has changed radically.

Conserving cash becomes the new mantra versus the rush to growth at any price, as they were fiercely promoting.

b. Closing a new round of financing may require entrepreneurs to accept terms they were not prepared for.

i. Down rounds

Down rounds are rounds of financing occurring when a startup offers shares for sale at a lower price than in previous financings. In good times down rounds reflect a lower trust from investors in the future of a venture, unrelated to the overall capital market movements. They are a rare occurrence among the total startup fund-raising deals. Since 2022 however, the proportion of down rounds has significantly increased, representing in the US 17% of all rounds in the third quarter of 2023.

ii. Cram Downs

A cram down is a more forceful situation when preferred shareholders not willing to provide additional capital are forced to accept a dilutive round. It plays in favor of the long-term success of the business, as both founders and employees remain motivated, unlike “passive investors” who are crammed down and lose their preference rights.

iii. Pay to Plays

This is the ultimate salvation financing, generally promoted by active investors ready to participate at the expense of passive investors, i.e. not participating in the round, who are asked to forego of their preference and have their shares immediately converted into common stock This often results in convincing shareholders to invest in the round at their pro rata and keep their preferred stock. Sometimes they may, alongside the lead active investors, benefit from better terms through the new series of preferred shares. Protracted negotiations make it a lengthy process, creating conflictual relationship between classes of investors. Their obvious benefit is that they provide capital when it is most required.

2. Valuations take a beating:

a. Confusing valuation increase with wealth building.

Founders too often are confusing the valuation of their venture at each round with their own wealth when the only valuation that should matter is the valuation at the time of exit (i.e. “the Liquidity Event”). Down rounds express a decrease in the valuation of the business at a certain period. It is still a round of financing, though, and the business remains a going concern while other founders in dire situation do not have this good fortune. Because building wealth is the main driver of entrepreneurship, a down round carries an unnecessary emotional weight. Many successful enterprises have experienced in their path to glory one or two backward steps that allowed to set the business back on its rails. Facebook is the most illustrious among them.

For entrepreneurs negotiating their maiden rounds, one cannot obviously talk of down rounds. However, what is certain is that the average pre-money valuation for early-stage startups, per industry, is lower in 2023 than it was in 2021. Rounds are not necessarily smaller, but the take from investors is higher. Let us say it is a down round in expectations. The big issue for founders is that business plans must show a prudent cash management when the equivalent plan, three or four years ago, would have focused on reaching the highest growth rate, regardless of the expense.

b. Is a down round a shameful stigma?

The quick response is no, it is not.

i. It allows to realign the business.

In many cases, a down round forces management to reassess objectives and align the company’s valuation with market conditions. Generally, it puts the venture back on new rails, sometimes with a faster growth in perspective.

ii. Listening to mermaids can be lethal.

Some entrepreneurs give credit to analysts and media who tout a coming improvement in the economic situation. In the hope for a future higher valuation, they would use any trick to maintain the illusion. In the US, SAFE (Simple Agreement for Future Equity) have been over-used, bringing third-rate investors to the table. Because the conversion price of the instrument is predicated upon the following round, it looks fair, and entrepreneurs keep their misplaced pride. Should we name them “down-to-earth rounds”?

We trust it is better for the startups shareholders to realign its valuation as soon as possible. The quicker it is accomplished, the higher the chances of successful subsequent financings.

iii. What matters is the valuation when a liquidity event finally occurs.

Watch out, unicorn founders and employees! Being overvalued will eventually catch up with you in the form of a failed financing. Nine out of ten unicorns are in a valuation bubble stage. The stage that follows a bubble is usually a crash. Yet, some will manage to survive. Those who bite the bullet, like Stripe, are set to resume their expansion.

3. Ventures with a runway under 18 months or less must take action.

It is well documented that running out of cash is a major cause of startup failures. This is truer in today’s uncertain environment.

In certain circumstances, founders can avoid a down round by focusing on reducing cash burn. Such discipline, though it is indispensable in developing a sustainable business, does not always extend the runway as expected. If practiced with a lack of discernment as to the impact on the employees’ morale, it may lead to skinning the operation to a point that prevents subsequent growth.

4. Happy are those with one or more anchor investors.

Anchor investors play a paramount role in the sequence of financing rounds. They are institutions or corporations with a flawless reputation. Their presence comforts new investors, as they are deemed to have proceeded with a thorough due diligence from which they draw a long-term commitment to the venture, becoming an agent of success on the management’s side. They enhance the team’s credibility, indirectly motivating new investors to participate in the current round.

a. Trust in the long-term perspective

This is really the strength of anchor investors. Not all startups attract investors with these qualities. Those that do are the top of the crop.

b. Positions are not frozen.

Other anchor investors may join, bringing a set of expertise that are crucial for further stages of growth.

5. Planning for a down round

There is no magic here. Good old business recipes to build a long-lasting company are coming back. Time-to-profitability must be short, implying a good control on costs and cash runway. Cash flow projections become again a major part of the CEO dashboard. But, first of all, communication channels with all stakeholders must remain wide open to prepare for a smooth understanding of the round by all parties and bring them on board.

a. The benefit of transparent communication.

i. With investors/shareholders

Managing a proper, regular communication with all shareholders helps them understand the issues while ensuring their confidence in the management and the business is not diminished. Unless the market conditions for the products and/or services your venture delivers have drastically deteriorated, there is no reason for them to suddenly doubt your ability to execute your plan.

ii. With employees

Addressing the issue of a potential down round upfront is the only way to retain key employees. Their dedication to the business often translates in an exceptional contribution during hard times. Concurrently, the board may be well advised to award options at a revised price.

iii. With Customers

You must absolutely avoid the feeling among customers that the prospects of one of their suppliers are dwindling. It is worth calling on each of them and pitch them the revisited growth story of your business and its cash standing.

b. Essential measures to take.

Undertake a thorough SWOT analysis to re-focus on products and services with the highest chance of growth within a short delay.

Hold off any hiring for long-term projects until your visibility in your cash generation is good enough.

Protect your cash flow by making use of factoring.

c. The role of the board

The board oversees the negotiation after deliberating and agreeing for the need to obtain equity financing. The board fiduciary duties imply that it should seek the best transaction possible for all shareholders, even if all classes of shareholders are not represented on the board. During the whole process up to the closing of the round, and including the acceptation of the term sheet, the board must disclose all material information relevant to the shareholders’ decision.

6. Down rounds in practice: how much can you surrender?

This is not about how much equity participating investors will take, but about the privileges attached to the investment in the round. Finding the right balance between preferences granted to investors and the minimum benefit you keep as a founder is not as hard as you think. Most startup investors are smart enough to understand that twisting the arm of entrepreneurs is not the best way to stimulate them. Traditional rights and preferences you are most likely to encounter, such as liquidation preferences in case of exit -including shutting down the company, rights of first refusal as a preemptive right of purchase shares in future offerings, as always, relate to the distribution of the proceeds between all shareholders in case of an exit. It is not trivial, particularly for companies that have gone through many financing rounds, as each new Series tend to provide special rights. It is quite like the inventory accounting method, LIFO (last in first out).

One must always keep in mind that any type of right can be negotiated. If your venture has already attracted many layers of investors, such negotiations are not straightforward. That is why it is recommended for boards, in down rounds, to proceed with a rights offering to all existing shareholders, in order to avoid potential conflict between participating and non-participating investors.

7. How long will this environment last?

a. Nobody can tell, except fools.

With uncertainties looming for 2024, in geopolitics, in the outcome of the US elections, and in the level of interest rates, even the best oracle would not venture to predict a return to a bull market this coming year, as it would not venture either to predict a bear market.

b. Plan for the worse

That is the surest way to have pleasant surprises.

Conclusion: Swings in markets are historically the norm

There is nothing to fear. Entrepreneurs who quickly adapt to a change in their environment tend to thrive in the long run. It is all about competition: when the market is high, investors compete to attract good startups. When the market reverses its course, entrepreneurs compete to get the good investors’ attention. Capital markets behave like any other market.